How Climate Risk Affects Valuation, Credit Risk, and Portfolio Management

- Kateryna Myrko

- May 16

- 4 min read

Climate risk is no longer just an environmental issue. For banks, investors, and companies, it can affect valuation, credit risk, capital ratios, collateral values, insurance protection, and portfolio allocation. In finance, climate risk matters when it changes expected cash flows, default probabilities, asset prices, or the cost of capital.

IFRS S2 explains that climate-related risks and opportunities are relevant when they could reasonably affect a company’s cash flows, access to finance, or cost of capital over the short, medium, or lo

ng term. That makes climate risk directly connected to valuation and financial analysis.

Real Data: Why Climate Risk Matters FinanciallyHow Climate Risk Affects Valuation, Credit Risk, and Portfolio Management

The financial numbers are already visible in official 2025–2026 data.

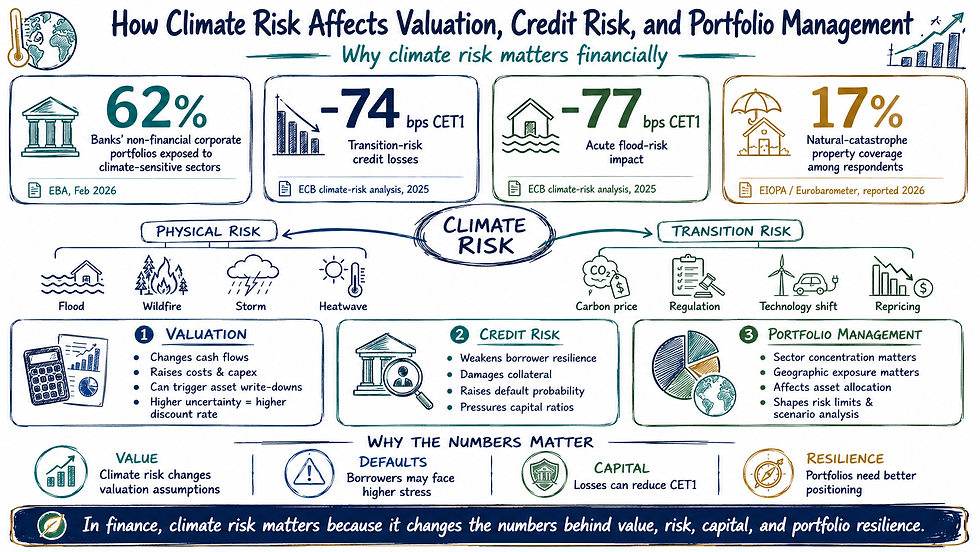

First, the European Banking Authority reported in February 2026 that banks’ exposures to sectors that significantly contribute to climate change remained around 62% of non-financial corporate portfolios. The EBA dashboard used data from a representative sample of nearly 120 large EU/EEA banks. This means climate-sensitive sectors are not a small niche; they represent a large part of real banking exposure.

Second, the ECB’s 2025 climate-risk stress-test analysis estimated that transition-risk credit losses reduced banks’ Common Equity Tier 1, or CET1, capital by 74 basis points over the 2025–2027 horizon. The same ECB analysis estimated that acute flood risk caused an additional 77 basis point decrease in CET1 ratios.

Third, insurance protection is weak. EIOPA stated in 2026 that only 17% of respondents in its 2025 Eurobarometer had coverage for property damage caused by natural catastrophes. For banks and investors, this matters because uninsured losses can reduce household wealth, weaken business recovery, pressure governments, and affect collateral values.

How Climate Risk Affects Valuation

Valuation depends on future cash flows, growth expectations, capital expenditure, risk, and discount rates. Climate risk can affect all of these.

For example, a company exposed to high emissions may face higher costs from carbon pricing, regulation, energy transition, or required investment in cleaner technology. A real estate company may face asset impairment if properties are exposed to flood, wildfire, or heat risk. A manufacturer may need higher capex to decarbonize factories or supply chains.

The effect on valuation can be direct: lower revenue, higher costs, higher capex, or asset write-downs. It can also be indirect: investors may apply a higher discount rate if they believe climate uncertainty makes future cash flows riskier.

In simple terms, climate risk changes the assumptions behind the valuation model.

How Climate Risk Affects Credit Risk

Credit risk is the risk that a borrower cannot repay debt. Climate risk can increase credit risk through both physical risk and transition risk.

Physical risk includes floods, droughts, storms, wildfires, and heatwaves. These events can damage assets, interrupt operations, reduce revenues, and weaken collateral.

Transition risk includes regulation, carbon prices, technology changes, market repricing, and changing consumer demand. For example, a borrower in a high-emission sector may face higher costs or lower demand if the economy transitions faster than expected.

The ECB’s 74 basis point CET1 impact from transition-risk credit losses is important because CET1 is a key banking-capital measure. The additional 77 basis point flood-risk impact shows that physical risk can also translate into credit losses, not just environmental damage.

How Climate Risk Affects Portfolio Management

Portfolio managers must think about climate risk at the level of sectors, geographies, companies, and asset classes.

A portfolio may be exposed to transition risk if it is concentrated in high-emission sectors such as energy, transport, heavy industry, real estate, or utilities. It may be exposed to physical risk if companies or assets are located in areas vulnerable to floods, storms, drought, or heat stress.

The Financial Stability Board explains that climate-related shocks can materialize through transition risks, such as abrupt changes in policy, technology, or consumer preferences, and through physical hazards such as floods, droughts, or windstorms. These shocks can be transmitted and amplified through the global financial system.

For investors, this means climate analysis can influence asset allocation, security selection, engagement, scenario analysis, and risk limits.

What Finance Professionals Should Watch

A practical climate-risk review should include emissions exposure, sector exposure, geographic exposure, insurance coverage, borrower resilience, transition plans, capex needs, and scenario results.

For banks, the key questions are: which borrowers are vulnerable, which collateral is exposed, and how could capital ratios be affected?

For investors, the key questions are: which assets are mispriced, which sectors face transition pressure, and which companies are better positioned for a changing economy?

Conclusion

Climate risk affects valuation by changing expected cash flows, costs, capex, asset values, and discount rates. It affects credit risk by influencing borrower resilience, collateral quality, default probability, and capital ratios. It affects portfolio management by changing sector exposure, geographic risk, scenario outcomes, and long-term allocation decisions. How Climate Risk Affects Valuation, Credit Risk, and Portfolio Management

The real numbers show why this matters: 62% of EU/EEA banks’ non-financial corporate portfolios remain exposed to climate-sensitive sectors, ECB analysis found 74 basis points of CET1 impact from transition-risk credit losses, 77 basis points from acute flood-risk effects, and EIOPA found only 17% natural-catastrophe property coverage among surveyed respondents.

In simple terms: climate risk matters in finance because it changes the numbers behind value, risk, capital, and portfolio resilience.

Comments